In the last year, the term “ecosystem” has finally made its way into the world of the insurance industry and almost in all board meetings. However, people in the industry frown at me when I utter the magic word “ecosystem”, don’t they?

It seems to me that ignorance around this topic has turned directly into scepticism. Maybe the term is just too hackneyed by now. Hardly any article (like this one) or any event can do without it. Perhaps companies talk too much about it and work too little on it!?

There might be another reason for this scepticism: C-levels at insurers and also some consultants are often of the opinion that insurers cannot or should not be in the centre of an ecosystem. So, there is no need to try it.

I absolutely disagree. Ecosystems are vital to the survival of insurance companies and also intermediaries. Therefore, they should enter the race for ecosystems now if they don’t want to leave the field to others.

First things first. What is an ecosystem?

The term ecosystem originated in ecology. In an economic context, the term ecosystem was first introduced in 1993 by James F. Moore in an article in Harvard Business Review magazine1.

An ecosystem bases on a cooperation of different companies from different industries around a specific topic. The goal of this network is to fully serve the customer at the centre with respect to this topic.

“In ecosystems, a different mathematics prevails: One plus one is more than two!”

An ecosystem will only be successful if the benefit in terms of its products and services is greater for the customer than the benefit from the products and services of the cooperation partners considered on their own. In other words, one plus one must be more than two.

An ecosystem is all about simplicity and convenience for the customer. Let’s take a look at some examples.

Some examples of ecosystems

Let’s start with the ecosystem “home”. There are numerous interlocking products and services around the topic of “apartment, house and yard”. These include, for example, security against burglary or the topic of “smart home”: in other words, the connected, intelligent house that makes everyday life easier.

This ecosystem also includes, for example, the early detection of damage to water pipes, the (automated) commissioning of necessary repairs, or a service for relocation or renovation. Products and services for the garden also play a key role. And ultimately, topics such as “home emergency call” and “meals on wheels”.

A craftsman’s service, a security service, a gardening professional and other partners could therefore join forces: They could offer the customer all products and services relating to “home” – all from a single source. In such an ecosystem, an insurance company and financial intermediary also have their place.

Other ecosystems are coming into focus in the insurance industry, too:

– Ecosystem “Mobility”: In this ecosystem everything turns on personal mobility. It is about public transportation, rental cars, air travel and, of course, insurance coverage – starting with accident coverage and (international) health insurance.

– Ecosystem “Health”: This ecosystem is all about the customer’s health as well as physical and mental well-being. Medical care as well as wellness, nutrition and sports play a key role here. This ecosystem is also about rehabilitation after an illness, but also about prevention and improvements of personal performance.

The “Finance” ecosystem

The ecosystem “Health” is likely to be primarily in the focus of a health insurer. Meanwhile, the ecosystem around finance is probably most exciting for a life insurer. When it comes to finance, almost everyone faces two basic fundamental problems:

- No clue about the current financial situation

- No idea what the options are

Various companies are already working on a solution to these two central problems. Specifically, they work on the ecosystem “Finance”. The result of this work will be a digital finance cockpit. With this cockpit, every customer will be able to capture the current financial situation at a glance and at any time. And every customer will be able to manage the personal finances either by themselves or with the help of an advisor.

Thanks to this cockpit, the customer is able to see how and where his financial resources are currently invested in short, medium and long term. Within this cockpit, it will be that easy to switch between the different “investment pots”.

Thanks to this cockpit, he will always have his overall investment risks in view. Advanced projections, which also take future income and expenses into account, give an indication of liquidity in the upcoming months as well as the potential future wealth.

“The ecosystem Finance with its financial cockpit will finally put

an end to people’s financial blindness.”

In the ecosystem “Finance”, technology ensures that the services “insurance” and “banking” are combined in a natural way. The boundaries between the individual insurance lines, which are completely unnatural from the customer’s point of view, will also disappear.

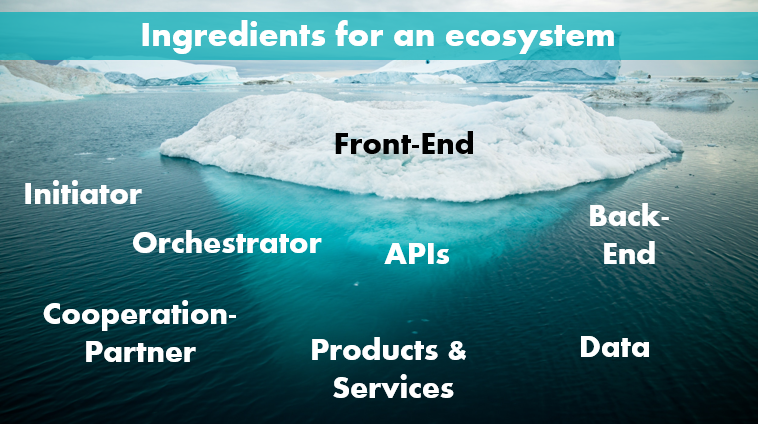

Roles and ingredients in the ecosystem “Finance”

The initiator of an ecosystem is the visionary. He has recognized that there must be an ecosystem around the specific topic of “Finance”. The initiator gives the starting signal for the development of the ecosystem.

The orchestrator is the architect of the ecosystem. He is expert of the specific topic and of the products and services of the ecosystem. The orchestrator designs the ecosystem based on this knowledge and the vision of the initiator. In doing so, he defines who is allowed to act in this ecosystem – and how. Initiator and orchestrator can also be identical.

“Initiator and orchestrator of an ecosystem can of course also be an insurer!”

Collaboration partners provide the individual puzzle pieces to the ecosystem’s value proposition. It is the puzzle of products, services and technology. So, in case of the ecosystem for finance for example, a puzzle of a savings account, life insurance products and financial advice.

In addition, collaboration partners can also bring customers into the ecosystem. For example, if a life insurer becomes partner in an ecosystem “Finance” all customers of the insurer will certainly be offered the complete services of the ecosystem – for example, savings account and credit card.

The back end is the technological backbone of the entire ecosystem. This is where all the information comes together. The front end is the face to the customer. In the ecosystem “Finance” the financial cockpit is the front end. It could be a portal and/or an app.

The interfaces (so-called APIs) connect the front end with the back end and all cooperation partners. This enables automatic communication in real time. Thus, a customer finds his current status of all products and services in the portal. For example, the current value of his fund units in the securities account.

Of course, the products and services are also important in an ecosystem. Without digital and simple products and services an ecosystem “Finance” will not work.

Data is also an important ingredient. An ecosystem is about serving the customer perfectly and holistically. To do so, the ecosystem needs to know the customer very, very well. Through their behaviour and interactions in the ecosystem, the customer directly provides the ecosystem with information. Thus, the ecosystem will understand the customer better day by day. This enables better service, which in turn translates into more information – a virtuous circle.

The race for the ecosystem “Finance” has already started

The pioneers are banks. In the last century, it was already possible to deal with almost all financial issues in their branches: from loans and savings account to fund investments and even insurance – bancassurance already was implemented at that time, somehow.

We therefore expect that banks are very open to such a digital ecosystem. Thanks to their numerous collaborations with FinTechs, they are probably also technologically prepared.

So, banks are probably in a pole position when it comes to the ecosystem “Finance”. And indeed, various surveys and market opinions see banks there.

On the other hand, a lot of trust has been lost among the financial crisis. The introduction of a “penalty interest rate” (they call it “fee”) and the cancellation of premium savings contracts also did nothing for the image. In addition, the customer experience at banks is probably stuck in the 80s and 90s of the last century.

So, it’s worthwhile for non-banks to enter the competition for the ecosystem “Finance”. Especially because the Payment Service Directive 2 (PSD2) allows non-banks to access the banks’ treasure: data.

This is where the various start-ups in the financial services industry, the FinTechs and InsurTechs, excel. However, the majority of these start-ups focus on the established players in the market as cooperation partners.

Only a very few are in direct competition with the top dogs. And these have already entered the race for the ecosystem “Finance”. I am talking of companies such as “Revolut” and “N26”, for example.

A life insurer also has a great interest in the ecosystem “Finance”. However, a life insurer today is primarily “only” a product supplier for “banks” and “brokers”. Therefore, few consider a life insurer to be actually relevant.

“The race for the finance ecosystem is an ultra-triathlon.

It is not important that you start first, but to start and then to finish.”

Asset managers are probably feeling the same way as life insurers. They tend to be in the background as suppliers to banks and life insurers. That’s why they are seen as a possible cooperation partner in the ecosystem and not as initiator or orchestrator, too.

The so-called “Big Techs”, i.e. large technology companies such as Google, have also entered the race. These Big Techs have several trump cards on their side: They have established customer networks and a great brand. They have customer data and contact. They have modern technology and they have a market size that exceeds the size of the established financial players many times over.

The fantasies of these Big Techs and the greed of their investors are forcing them to grow more through innovation and by deepen the value chain. The latter will inevitably come at the expense of established players in the financial industry.

Google, for example, not only has its own payment service Google Pay, but has also an e-money license and a PSD2 license in the EU2. With a few banks as cooperation partners, Google also launched an account service last year3. It seems that Google is building an ecosystem “Finance” around its payment service. The other Big Techs like Amazon and Facebook are no less buzzy on this topic2.

Some thoughts

1. Insurers need to finally get into the ecosystem race

An insurer can either build an ecosystem itself or cleverly integrate into an existing or emerging ecosystem. In my view, an insurer should do both and simultaneously. For example, a life insurer could try itself at the ecosystem “Finance” and, in parallel, become involved in an ecosystem “Health”.

In both cases, the basic prerequisite is that all internal processes are automated. Thus, it is possible to connect easily to the ecosystem and the other cooperation partners. For many insurers, however, this is still a pipe dream – and it is precisely here that companies need to do their homework.

Life insurers in particular are lagging behind, for example in product development. It can take two years for a new product to be developed and made available to the sales channel. In an ecosystem, innovation and speed are key. Anyone who is not able to deliver will simply be left out.

Whether the insurer wants it or not, ecosystems are already be formed around its existing customers. And if the insurer does not play along in these ecosystems, it will lose its customers in the medium term.

An ecosystem acts like an invisible wall. If the customer is in the ecosystem and satisfied, he will stay in it. Because there is simply no reason for him to turn to another ecosystem. Ecosystems are the only way to achieve eternal customer loyalty. In building an ecosystem, most InsurTechs are a tool for an insurer to use at all costs.

2. An insurance intermediary needs to build its own “Finance” ecosystem and within it, he will transform himself into an omnichannel financial advisor.

Traditional insurance intermediaries still have a crystal-clear advantage: customer contact.

They have built up and maintained this contact over many years, even decades. This customer trust is a very, very valuable asset. It currently secures the insurance intermediary the pole position with the customer. But this pole position must be defended – against other market participants and against other emerging ecosystems. He will only succeed in this with its own ecosystem “Finance”.

Thanks to digitization and new players in the market, the range of financial products is increasing. Given the current financial knowledge of the population, some form of advice will continue to be necessary in the future. This advice must be holistic and has to cover all financial areas.

3. The Insurance Service Directive is coming

With the Payment Services Directive (PSD2), the legislator has made a significant contribution to the establishment of an ecosystem “Finance”. PSD2 requires banks to provide interfaces through which other service providers can access customers’ account data with their consent. Account data is an elementary ingredient in an ecosystem.

It is only a matter of time before the insurance industry faces similar regulation. Then insurers will also have to open the doors to their well-guarded black box and customer data to other service providers. This not only adds a new dimension to transparency and comparison options. It also finally paves the way for a complete ecosystem “Finance”.

4. It is like the Monopoly game: In the end, only one can win

The number of successfully running parallel ecosystems on the same topic – for example “Finance” – is likely to be very, very limited. An ecosystem will only be successful if it scales. Only then the virtuous circle of “more customers and more data provide more customers and more data” help the ecosystem to grow exponentially. An established ecosystem can then only be replaced with a great deal of effort. Just imagine the effort that would be required to seriously compete with Amazon and its ecosystem.

However, it is also clear that a handful of ecosystems “Finance” will ultimately also need just a handful of banks and insurers. The harmonization of the financial world in the EU will additionally enable cross-border ecosystems. And this will fuel the very big wave of consolidation in the financial service industry.

Sources

1 https://hbr.org/1993/05/predators-and-prey-a-new-ecology-of-competition

2 https://www.moneytoday.ch/news/big-techs-und-fintechs-werden-im-finanzbereich-sichtbarer/

3 https://www.it-finanzmagazin.de/google-pay-wird-zur-online-banking-zentrale-109715/